Part V of The Basics of Commercial Lines Rating covers how to read a WSRB loss cost publication.

As a WSRB Subscriber, you’ve probably used our Risk Search tool to find Basic Group I (BGI) loss costs for specifically rated properties. But do you know what all that information means? If not, read on. We’ll review a typical WSRB loss cost publication to help fill in the blanks.

As we learned in Part I of the Commercial Lines Rating Series risks not eligible for class rating must be specifically rated. Specific rating refers to a specific building and applies to the structure and its contents. Specific BGI loss costs are usually associated with larger businesses or those involved in hazardous operations.

An on-site inspection of the property is required to develop specific BGI loss costs. After the inspection, we create a loss cost publication that reflects the information the inspector finds.

Related:

WSRB's Essential Guide to Commercial Property Risk Assessment

Loss cost publications commonly include

- Advisory Prospective Basic Group I loss costs applicable to the causes of loss, (frequently referred to as perils) of fire, lightning, explosion, vandalism, and sprinkler leakage.

- Loss costs are displayed as annual and apply per $100 of insurance.

- An assumed minimum deductible of $500 and 80% coinsurance, unless otherwise specified.

- A base Limit of Insurance (LOI) of $250,000 for the building and $50,000 for contents. Note that limits of insurance other than the base limits will require the application of LOI relativity factors. LOI and base limits went into effect July 1, 2013, so loss costs calculated prior to this are displayed separately and do not require LOI relativity factors to be applied.

Your loss cost publication will also feature

- Building description, which tells you a little about the building. In the example publication below, you’ll see the structure is 27 stories and constructed of glass and metal. If a symbol such as /1/, is shown in this area and in the Occupancy Type Description, required clauses, warranties, or rule provisions apply. (/1/ means a Protective Safeguards Endorsement must be attached to the policy).

- Sprinkler Credit which shows you whether the building is sprinklered or non-sprinklered. The building below is Non-Sprinklered, which means it doesn’t qualify for credit.

- CSP refers to the four-digit Commercial Statistical Plan Classification Code that identifies the type of business conducted in that building. Again, specific loss costs generally apply to large businesses or any size building that is conducting hazardous operations.

- RCP stands for Rating, Construction, and Protection. This little number is packed with lots of valuable information.

- The schedule identifies the classification of the property. This building’s BGI loss cost is developed using Schedule 02, Light Non-manufacturing Occupancies.

Related:

Rating Commercial Property

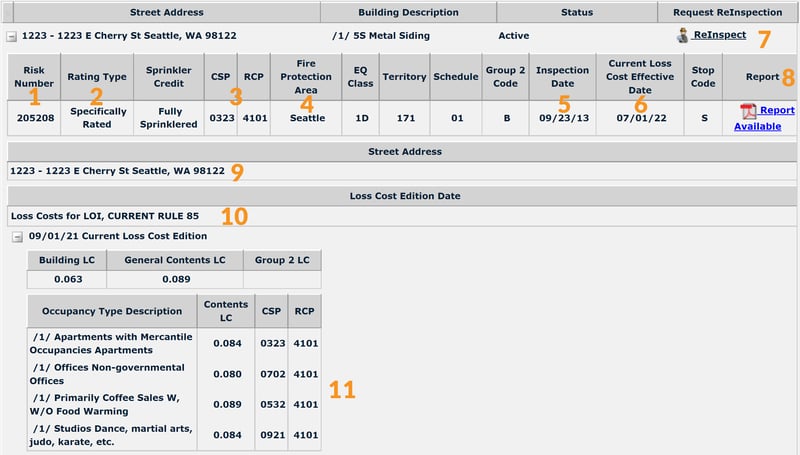

A sample loss costs publication

Take a look at the orange markup on our sample publication. An explanation of each field is included in the legend.

|

1 |

Risk Identification Number |

|

2 |

Indicates if risk is class rated or specifically rated |

|

3 |

Building CSP and RCP Codes |

|

4 |

City or Fire Protection District where the property is located |

|

5 |

Group II CSP Code |

|

6 |

Effective date of most recent change. “S” in Stop Code means the effective date is a General Revision |

|

7 |

Link to request a reinspection |

|

8 |

Link to Underwriting Report |

|

9 |

All known Street Addresses for the Building |

|

10 |

Loss cost Edition – effective date of General Revision (Several previous editions may also be shown for other than LOI loss costs) |

|

11 |

Individual Occupants of the Building. Note: Symbols, such as /1/, will be shown here and in the Building Description. |